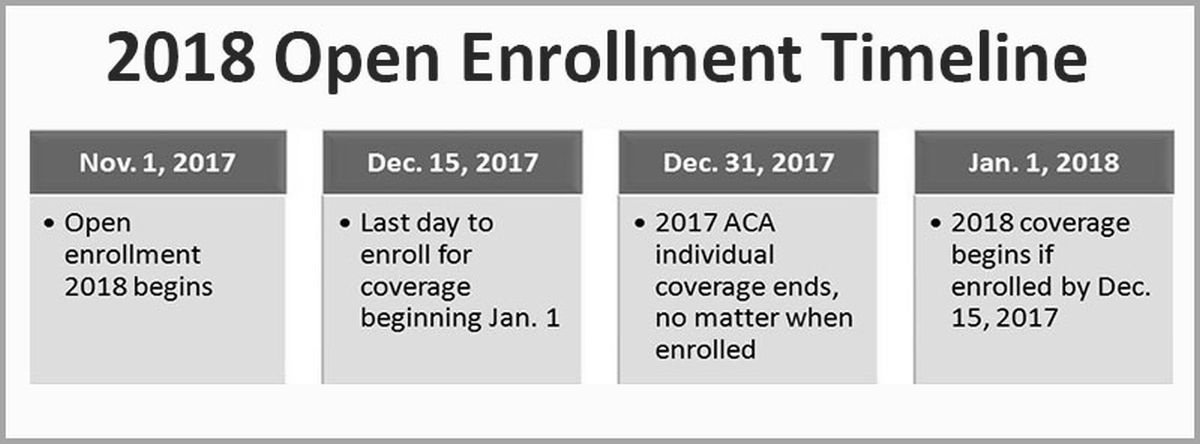

Open enrollment for individual health coverage begins November 1st 2017 and ends December 15th 2017. During this period you can join a health plan, renew your current plan, or change to a different plan.

As you may already have heard the cost of health insurance have skyrocketed under ACA regulations, and 2018 is no exception. Many individuals have seen 25-50% annual increases since the major parts of the ACA regulations went into effect. While much can be debated about who is to blame for the increases and what should be done to fix the failed system, the problem remains none the less; However, many are not feeling the effects of these increases due to Medicaid expansions and Health Exchange Subsidies. For those receiving APTC (Advanced Premium Tax Credits) basically the increases go largely unnoticed based since the premiums can not exceed a percentage of their income; Therefore, the subsidy increases to offset the cost increases.

Example: Family of four – parents aged 42 earning 60,000 with two minor children could expect to receive about $600 a month in APTC toward their insurance premiums. and the average Silver plan might cost them $400 a month. The true cost of the plan is $1000 a month, so if they have a 25% increase in premiums the cost of the plan would be $1250 the next year, but their APTC would also increase to $850 so their cost is still $400 a month.

For the families receiving the assistance everything is fine, but for those families earning even $1.00 over the limit they receive nothing. For example that same family who worked hard now received raises they earn $98,000 and are no longer receiving assistance in addition to their higher tax bracket (let’s say 25%) and is not receiving the equivalent of $12,750 after tax funds in their budget. They work twice as hard to go from bringing home $51k (60k at 15% tax bracket) to bring home about $63k (25% tax bracket and loss of APTC).

The problem gets even worse for seniors!

Example: Empty nest couple age 63 earning the same $60,000 would receive about $1000 a month and would still be responsible for about $500 of the premium; However, if they earn just $5000 more due to salary increases, stock dividends, or just about any other taxable income – They receive nothing and they pay the full $1500 a month. Keep in mind you are projecting income on the application for APTC not reporting what you have already earned! Just to recap for earning just $5000 more than expected they will actually lose more than $7000 in take home money.

So what can we do?

Well… we don’t make law here at Cunningham Insurance, we only work for our clients to make sure they are working within the system to help them find the solution that works best for them.

A couple of solutions for clients that are not currently qualifying for assistance:

- We work together with your tax professional to see if there is any way we can reduce your MAGI (Modified Adjusted Gross Income) to bring your income down to a level that qualifies you for APTC.

If you are like the senior couple that is only a few thousand from qualifying for the help we can look at funding an IRA, Solo K, or SEP. By max funding two IRA’s (husband and wife) with $12,000 going into the IRA your income is reduced by the same amount and you now qualify for the APTC and you have a little more for retirement.

If you are Self Employed we can fund a SEP up to $54,000 a year for both 2017 and 2018.

These are just a few ideas that we have used to make your health care more affordable.

2. Can’t make APTC work for you and can’t pay for the high price of Health Insurance (or don’t want to)?

Consider Medi Share plans they will help you avoid the Tax Penalty (2.5% of you income) for not having insurance. While they don’t have the same grantees that insurance carriers can offer, they can provide a viable alternative to health insurance at a fraction of the cost.

3) Short Term Medical insurance has been an option in the past but in May of 2017 the HHS mandated that all STM plans terminate after 3 months, but with President Trump’s recent executive order on health care it looks like that option may be made available again. This is could be a good alternative for healthy individuals that don’t require continuous care for an existing medical condition. They currently do NOT cover preexisting conditions.